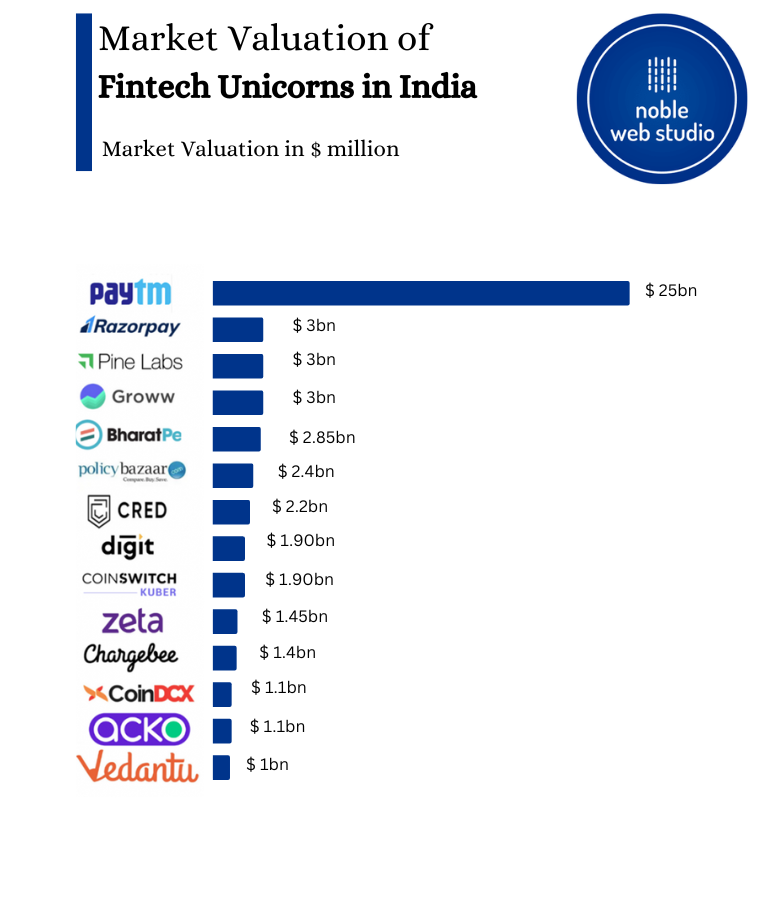

This is the era of startups, and financial technology or fintech makes up a massive portion of these up-and-coming businesses. It is no secret that we’re moving towards a largely cashless society, and thanks to fintech startup like Aadhaar Enabled Payment System (AePS) even India’s rural regions are catching up at a swift pace. Hence, it is not strange to want to join this race and contribute to the development of fintech in India.

Many aspirants who want to start a fintech startup might lack the knowledge of how to go about executing it. This article will try to answer all your questions– legal or practical.

4 Crucial Steps for Starting a Fintech Startup in India:

- Choose a Business Model that Works for You

- Choose The Type Of Fintech You Want To Invest In

- Deal With All The Legal Requirements

- Register Your Intellectual Properties and Domain

Step 1 – Choose a Business Model that Works for You

Finding the right business model can become the most crucial decision for your fintech startup. Three basic types of business models are popularly used for fintech in India. Your business can be a One-Person Company (OPC), Limited Liability Partnership (LLP), and Private Limited Company (PLC) on the basis of ownership and liability.

I. One-person Company (OPC):

In 2013 India introduced the Company’s act, making it possible for only one person to start a company. You can be the sole owner of your fintech startup, and solely direct the ongoing operations of the company.

II. Limited Liability Partnership (LLP):

It is an alternative business model that limits the liability placed on a partner. LLP is a legally independent entity that can exist irrespective of changes in partners, making it so that the partners are liable, only for the contribution they made. This is sustained through legal agreements. The LLP model makes sure that a fintech startup survives succession, making it a popular choice for fintech in India.

III. Private Limited Company (PLC):

It is arguably the most widely known business model for fintech startups, as it can be established with just two partners, unlike public limited companies that require a minimum of seven people in partnership. A private limited company can be expanded to two hundred partners.

Step 2 – Choose the Type of Fintech You Want to Invest In

There are a few popular and prominent types of fintech businesses that are dominating the market in India, making it high time for startups and investors to venture into these fields. These are:

I. Digital Lending/ Peer-to-Peer Lending:

This type of fintech allows consumers to take loans through their phones, bypassing the lengthy procedure of traditional bank loans. It is one of the most progressive sectors of fintech in India.

II. Digital Payment:

Payment portals like AEPS, Bharat Bill Pay (BBPS), Unified Payments Interface (UPI), etc., come under this sector. If you want to start a business in the digital payment sector, software solutions providers like Noble Web Studios can help design and establish your new business.

III. Crowd Funding:

Crowdfunding websites and apps like Milaap.org and GoFundMe are also considered fintech. While these are examples of humanitarian crowdfunding, some platforms allow entities to raise money for business ventures.

IV. Stock Trading Apps:

These platforms enable users to buy and trade stocks, reducing the complexity of the process. Apps like 5 paise and Upstox are two examples of this kind of fintech.

Step 3 – Deal with All the Legal Requirements:

It goes without saying that until and unless one has extensive experience in financial law, it is impossible to navigate all the legal requirements of starting a fintech startup on their own. You need a trustworthy lawyer and an accountant to make your venture successful. When it comes to fintech in India following requirements can be observed:

- Co-Founders Agreement: It is a legal contract that maps out the responsibilities of each co-founder, states their financial contributions, and checks their risk factors.

- Name availability Verification: This helps in verifying whether your fintech startup has a unique enough name for registration.

- Register with the Ministry of Corporate Affairs (MCA): Regardless of your business model, to start a business in fintech in India, you need a Business Incorporation Certificate. MCA provides this certificate upon registration.

- Establishment/Trade License: If your organization has more than ten employees, you need a license from the governing body to set your business establishment up on a particular premise.

- Obtaining a Permanent Account Number (PAN) and Tax Deduction Account Number (TAN): TAN & PAN are mandatory for operating any business in India. Issued by the Income Tax Department these two should be on the top of your priority list while starting a fintech in India.

- Register for Goods and Service Tax (GST): Business entities must register for GST and fintech startups are no exception to it. One must register their fintech startups through the registration portal and obtain a six-digit Goods and Service Tax Number (GSTN).

- Employees State Insurance (ESI): Established to protect the right of an employee, this requires business entities to pay the insurance premiums of the employees. If you plan to hire employees for your fintech startup, ESI registration is mandatory.

- Employees Provident Fund (EPF): This is only applicable to your establishment if you plan to have more than 20 employees. This scheme mandates that the companies cover employees who make less than Rs. 15,000, in a month.

- Digital Signature Certificate (DSC): To establish a fintech startup in India, or any company for that matter, you will need to acquire a Digital Signature Certificate (DSC). This DSC will ensure the safe transaction of documents online, and hence, should be present in all official documents.

Step 4 – Register Your Intellectual Properties and Domain:

Even when you are investing exclusively in fintech in India, it is prudent to remember that aesthetics are still important in tech businesses. Your business will have a lot of unique factors that you need to protect, as these factors are crucial to its existence in the market. To safeguard your brand name, website, mobile applications, tagline, etc., you need to secure Intellectual Property Rights (IPR) by registering them.

In today’s day and age, a company cannot be ‘Fintech’ until and unless it exists online. You will have a web portal of your own regardless of the type of fintech startup you plan to establish. You need to obtain a domain to protect your company in cyberspace; this will include the website, phone app, and other associated web space you wish to occupy.

To Conclude:

Industry experts have continuously predicted that fintech will keep growing in the future, and with the onset of the New Year, it can be said that these experts are yet to be proven wrong. So, if you are contemplating starting a fintech startup, now is the best time, and your business will thrive in these optimal conditions.

And if you are set on investing in a digital payment platform, book a demo with Noble Web Studios, to expand your options and get the best possible service in the market.