In today’s fast-moving digital world, easy access to banking services is more important than ever. Micro ATM machines are helping bridge the gap, especially in rural and remote areas where traditional bank branches may not be available. If you’re a business owner, retailer, or fintech enthusiast looking to offer banking services like cash withdrawal, balance inquiry, or fund transfer, Micro ATMs can be a powerful solution.

Micro ATM, also known as mini or mobile ATMs, are portable point-of-sale (POS) terminals that enable basic banking transactions in remote or underserved areas. These devices are vital for financial inclusion, offering services like cash withdrawals, balance inquiries, and fund transfers, especially where traditional ATMs are scarce. They are typically used by banking correspondents or agents and connect to banking networks via GPRS, 3G, or 4G, ensuring reliable operation even with limited internet access.

In this blog by NobleWebStudio, we’ll explore the key features of Micro ATM machines, how they work, and why they are becoming an essential tool in financial services across India. Whether you’re planning to start a money transfer business or expand your digital service offerings, understanding these features will help you make smart decisions.

What is a Micro ATM Machine?

A Micro ATM is a handheld, portable device that works as a mini-ATM, enabling basic banking transactions like cash withdrawals, deposits, and balance inquiries, especially in remote or underserved areas where traditional ATMs are scarce. These devices, resembling point-of-sale terminals, connect to the bank’s network through GPRS to process transactions.

Here’s a more detailed explanation:

Integration with AEPS: Micro ATMs often connect with the Aadhaar Enabled Payment System (AEPS), allowing for transactions based on Aadhaar authentication.

Functionality: Micro ATMs allow users to conduct common banking transactions, such as cash withdrawals, deposits, and balance inquiries, using a debit card.

Accessibility: They are particularly helpful in rural areas or locations with limited access to traditional bank branches, expanding financial inclusion.

Technology: Micro ATMs are typically handheld devices that use card swipe and fingerprint authentication (often linked to Aadhaar) for secure transactions.

Business Correspondents: These devices are often operated by Business Correspondents (BCs), who are trusted individuals that provide banking services on behalf of banks.

Cost-Effectiveness: Micro ATMs help lower the operational costs associated with traditional ATMs, making them a viable option for expanding banking services.

Transaction Limits: While they can handle significant transaction volumes, there might be daily or transaction-based limits on cash withdrawals.

Security: Micro ATMs ensure security through fingerprint authentication and other measures to protect against fraud.

Micro ATM Machines Work?

Micro ATMs are like modified point of sales terminals. This terminal can connect to the banking network via GPRS to perform banking transactions. This machine contains a card swipe facility. This initiative aims to bridge the gap between the need and availability of cash requirement in the eco-system.

Here’s how they typically work:

1. Device and connectivity

- Micro ATMs are handheld devices used by authorized agents, often called Business Correspondents (BCs).

- They connect to the bank’s network via mobile data (GPRS, 3G, or 4G) to process transactions in real-time.

2. Customer verification and transaction initiation

- The customer visits a banking agent with a micro ATM at a local shop or designated location.

- To start a transaction, the customer’s identity needs to be verified using either a debit card and PIN or their Aadhaar number with biometric (fingerprint) verification.

3. Transaction processing

- After verification, the customer selects the preferred transaction, such as cash withdrawal, balance inquiry, or fund transfer.

- The micro ATM submits the request to the bank’s server for approval.

- The bank verifies the customer’s details and reviews account balance.

4. Transaction completion

- If authorized, the micro ATM operator hands over the cash to the customer (for withdrawals).

- A transaction receipt is created, confirming the transaction details.

- Both the customer and the bank get confirmation of the completed transaction.

Read Blog : Micro-ATMs: The Ultimate Solution for Seamless Banking Transactions

Why Are Micro ATM Machines Important?

Micro ATMs offer a range of banking services, ranging from basic transactions like cash withdrawals and balance inquiries. They also offer more advanced functionalities such as mini statements and fund transfers. Moreover, they facilitate Aadhaar-enabled payment services.

Here’s why they are important:

- Financial Inclusion: Micro-ATMs bridge the gap between traditional banking and underserved communities, bringing banking services closer to rural populations who might not have direct access to bank branches or regular ATMs.

- Convenience: They allow people in remote areas to withdraw cash, check balances, transfer funds, and access other basic banking services locally, eliminating the need to travel long distances for such transactions.

- Cost-effectiveness: Setting up and maintaining micro-ATMs is significantly cheaper compared to traditional ATMs, making them a more practical option for banks and financial institutions to deploy in remote areas.

- Employment opportunities: Micro-ATMs create opportunities for local business correspondents (BCs) and shop owners to become agents, providing banking services and earning commissions on transactions.

- Supporting Government Initiatives: They support the distribution of government benefits, subsidies, and welfare payments directly to beneficiaries, promoting transparency and reducing reliance on intermediaries.

- Digital Literacy: As people engage with micro-ATMs, they become more comfortable with digital transactions, promoting financial literacy and the adoption of digital payments.

- Stimulating Local Economy: By making financial transactions easier and more accessible, micro-ATMs boost economic activity and growth within rural communities.

Examples

- For instance, Noble Web Studio offers Micro ATM machine allows customers to withdraw cash using a debit card, even in the absence of a nearby ATM.

- Noble Web Studio is a fintech solution provider that enables secure and seamless banking transactions through its micro ATM technology.

Micro-ATMs are playing a key role in India’s journey towards financial inclusion and a digital economy by making banking services accessible, secure, and convenient for a wider population.

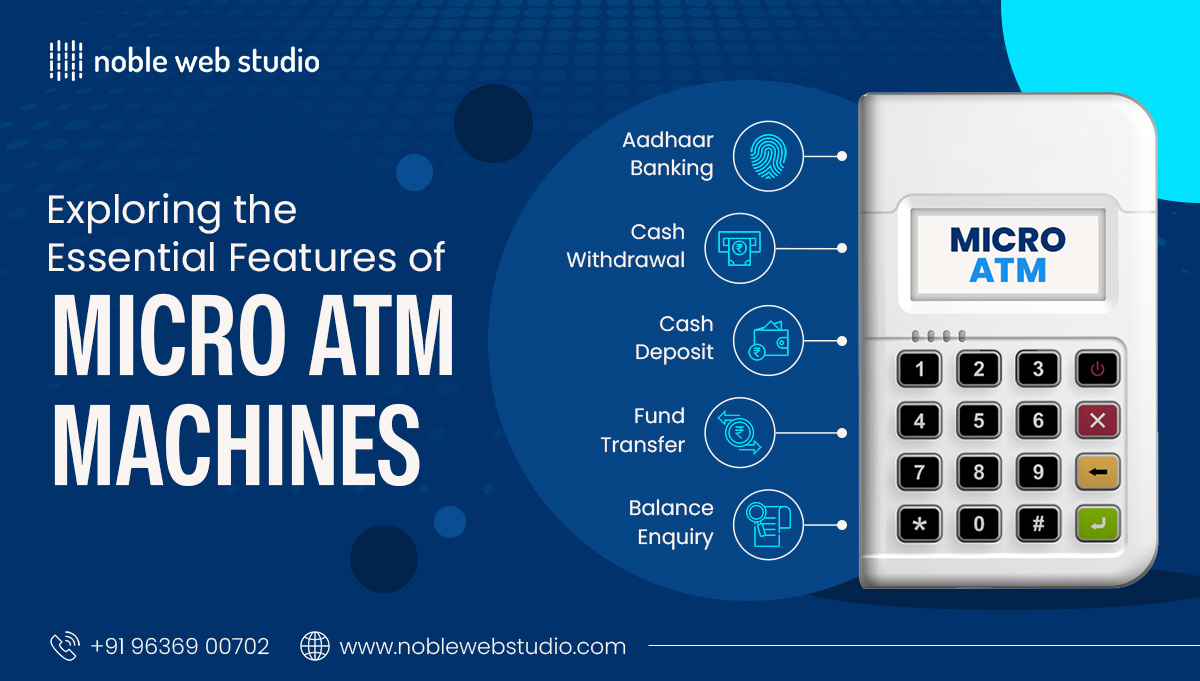

Features of Micro ATM Machines

Micro ATMs are portable devices that bring basic banking services to underserved areas, working as mini-ATMs or Point-of-Sale (POS) terminals. They enable cash withdrawals, balance inquiries, fund transfers, and mini-statements, often using Aadhaar-enabled payment systems AePS for secure transactions.

Here’s a more detailed look at their features:

Key Features:

- Portability: Micro ATMs are compact and easy to carry, allowing agents to provide banking services in various locations.

- Biometric Authentication: They often include fingerprint scanners for secure transactions via AePS.

- Connectivity: Micro ATMs utilize GPRS, 3G, or 4G to connect to bank networks, enabling functionality even in areas with limited internet.

- Basic Banking Services: They support essential transactions like cash withdrawals, balance inquiries, money transfers, and mini-statements.

- Aadhaar Integration: Many micro ATMs in India leverage the Aadhaar Enabled Payment System (AePS) for secure and convenient transactions.

- Payment Options: They often support both card-based and Aadhaar-based transactions.

- Mini-statement generation: Provides a short history of recent transactions.

- Thermal Printer: Many models include a thermal printer for generating transaction receipts.

Read Blog : Features of a Reliable Micro ATM Service Provider

Micro ATM Machine Benefits

Micro ATMs offer several benefits, including increased financial inclusion, easy access to banking services, and lower costs compared to traditional ATMs. They also promote digital transactions and facilitate the disbursement of government benefits.

Here’s a more detailed look at the advantages:

1. Enhanced Financial Inclusion:

- Micro ATM extend banking services to remote and underserved areas, bringing financial services to those who previously lacked access.

- They help bridge the gap between traditional banking and the unbanked or underbanked population, particularly in rural areas.

- By providing convenient access to cash and other banking services, micro ATMs can empower individuals and communities economically.

2. Convenience and Accessibility:

- Micro ATM offer a more convenient and accessible way to perform basic banking transactions like cash withdrawals, balance inquiries, and fund transfers.

- They eliminate the need to travel long distances to bank branches or traditional ATMs, saving time and effort.

- Micro ATMs are often available 24/7, providing continuous access to cash and other services.

3. Cost-Effectiveness:

- Micro ATMs are generally less expensive to deploy and maintain than traditional ATMs, making them a more affordable option for banks and financial institutions.

- The lower cost allows for wider deployment, especially in areas where traditional ATMs might not be economically feasible.

- This cost-effectiveness also translates to lower transaction fees for users.

4. Promoting Digital Transactions:

- Micro ATMs facilitate digital transactions by enabling electronic payments and reducing reliance on cash.

- They can be used for various digital payment methods, contributing to the digitization of financial transactions.

- This can lead to greater transparency and efficiency in financial dealings.

5. Supporting Government Initiatives:

- Micro ATMs play a crucial role in disbursing government benefits, subsidies, and welfare payments directly to beneficiaries.

- This ensures that social welfare programs reach the intended recipients efficiently and transparently.

- Micro ATMs can also be used for other government-related transactions, such as tax payments or utility bill payments.

6. Security and Reliability:

- Micro ATMs often incorporate biometric authentication features, such as fingerprint scanners, to enhance transaction security.

- This helps prevent fraud and unauthorized access to accounts, ensuring the safety of financial transactions.

- Micro ATMs also offer real-time transaction updates, providing transparency and accountability for both customers and banking agents.

Types of Micro ATM Machines Available in the Market

Different types of Micro ATM machines are available in the market, catering to various needs and functionalities.

Types Micro ATM Machines

- Basic Micro ATMs: These are simple, low-cost devices primarily offering cash withdrawal and balance inquiry services.

- Aadhaar Enabled Payment System (AEPS) Micro ATMs: These machines facilitate transactions using Aadhaar numbers and biometric authentication (fingerprint scan), eliminating the need for debit cards.

- MPOS (Mobile Point of Sale) Micro ATMs: These are portable, handheld devices that connect to smartphones or tablets via an app to process payments and offer banking services.

- WiFi POS Micro ATMs: These Micro ATMs connect to banking networks via WiFi, supporting cash withdrawals and balance inquiries.

- Integrated Micro ATMs: Some Micro ATMs are integrated with other devices like thermal printers and fingerprint scanners to offer more comprehensive banking solutions.

Popular provider and models

- Noble Web Studio offers advanced Micro ATM solutions, including Aadhaar-enabled Payment System (AEPS) devices, EDC machines, and POS swipe machines for seamless cash withdrawals, balance inquiries, and sales transactions. These devices come with affordable pricing, real-time commission updates, and Bluetooth connectivity for ease of use. Additional features include money transfer, mobile recharge software, and bbps bill payments, making them an all-in-one solution for digital banking services.

How Micro ATM Machines Facilitate Cash Withdrawal and Deposits

Micro ATMs are portable, handheld devices that act as mini versions of traditional ATMs. They’re designed to bridge the gap in banking accessibility, particularly in remote and underserved areas where traditional ATMs and bank branches are scarce.

Here’s how they facilitate cash withdrawals and deposits:

1. Cash withdrawals

- Authentication: Customers authenticate themselves using either their debit card and PIN or their Aadhaar number and biometric verification (fingerprint or iris scan).

- Transaction Processing: The micro ATM connects to the bank’s system (often using GPRS) and processes the withdrawal request.

- Cash Disbursement: An authorized business correspondent (BC) operating the micro ATM hands over the requested cash to the customer.

- Confirmation: Both the customer and the bank receive confirmation of the transaction.

2. Deposits

While traditionally focused on withdrawals, some micro ATMs and related services are evolving to include deposit functionalities:

- Cash Acceptance: Some micro ATMs can accept cash deposits.

- Account Credit: The deposit amount is credited to the customer’s account in real-time or near real-time.

- Potential limitations: Deposit functionalities might still be less prevalent than withdrawals, and specific limitations or procedures could vary depending on the service and the type of micro ATM.

Key features and benefits of micro ATMs

- Portability: Their compact size allows BCs to easily carry and operate them in various locations.

- Financial Inclusion: They empower individuals in remote areas with access to basic banking services, fostering financial inclusion.

- Cost-Effectiveness: Micro ATMs are generally cheaper to deploy and maintain compared to traditional ATMs, making them a viable option for banks to expand their reach.

- Security: They incorporate security measures like biometric authentication and PIN verification to ensure secure transactions.

- Interoperability: Many micro ATMs work with debit cards from various banks and support the Aadhaar Enabled Payment System (AePS) for Aadhaar-based transactions.

In essence

Micro ATMs serve as a crucial tool in expanding banking services to remote and underserved areas, facilitating cash withdrawals and, increasingly, deposits, thereby contributing significantly to financial inclusion and the growth of digital payments.

Supported Transactions and Services on Micro ATM Machines

Micro ATMs support various essential banking transactions and services, particularly in areas with limited access to traditional banking infrastructure. These handheld devices typically allow for:

- Cash Withdrawal: Customers can withdraw cash using their debit card or Aadhaar number for biometric authentication. The maximum limit for cash withdrawal at a Micro ATM is often ₹10,000 per transaction. Noble web studio mention a daily limit of ₹20,000 for their Micro ATMs. The monthly limit via AePS is generally 10 transactions or ₹50,000, whichever is breached earlier.

- Balance Enquiry: Users can check their account balance using their card and PIN or Aadhaar and biometric authentication.

- Fund Transfer: Transferring funds between bank accounts is also a supported service. The daily limit for fund transfer transactions is usually ₹10,000 per day per customer.

- Mini Statement: Micro ATMs can provide a mini statement displaying the last few transactions from the account.

- Aadhaar Enabled Payment System (AePS): This allows users to conduct banking transactions (deposit, withdrawal, balance inquiry, fund transfer) using their Aadhaar number and biometric authentication.

- Cash Deposit: Noble web studio micro ATM solution also support cash deposits, where the customer gives cash to the business correspondent (BC) operating the Micro ATM, and the corresponding amount is credited to the customer’s account.

- Bill Payments: Micro ATM platforms offer bill payment services for utilities and other bills.

In essence, Micro ATMs serve as an important tool for financial inclusion by providing accessible banking services, especially in areas with limited infrastructure.

Security Features of Micro ATM Machines

Micro ATMs are designed to provide basic banking services in remote or underserved areas, and their security is crucial for safe and reliable transactions. To protect users from fraud and unauthorized access, micro ATMs incorporate a range of security features:

1. Biometric authentication

- Many micro ATMs use fingerprint scanners for verifying identity, replacing or supplementing the need for a PIN.

- Some models may also integrate iris scanning or other biometric technologies for enhanced security.

- The Unique Identification Authority of India (UIDAI) has also implemented a security mechanism for Aadhaar-based fingerprint authentication to detect spoofing attempts.

2. Secure PIN pad

- Encrypted PIN pads ensure that the PIN entered by the customer is immediately encrypted and locally processed, minimizing the risk of PIN theft through electronic means.

- Users are also advised to cover the keypad while entering their PIN to prevent shoulder surfing or hidden camera attacks.

3. Encryption technology

- Micro ATMs employ encryption techniques to secure sensitive data, such as card numbers and personal details, during transmission between the device and the banking network.

- Encryption converts data into unreadable text, making it difficult for unauthorized parties to intercept and interpret the information.

- Advanced Encryption Standard (AES) is a modern encryption method adopted for securing financial transactions.

4. EMV chip card acceptance

- Micro ATMs are increasingly being upgraded to accept EMV chip-based cards, which are more secure than magnetic stripe cards and significantly reduce the risk of card cloning and counterfeit fraud.

- The EMV standard requires banks to implement strict security controls for card payments, including encrypting cardholder data and restricting physical access to the devices.

5. Secure communication channels

- Micro ATMs utilize encrypted communication channels to transmit transaction details to the bank’s server via mobile networks or GPRS connections.

- This prevents data interception during the transaction process and ensures the integrity and confidentiality of the information.

6. Anti-skimming and anti-tampering measures

- Micro ATMs are often equipped with anti-skimming devices that detect and block unauthorized skimming attempts.

- These devices may also include sensors that emit signals to disrupt skimmers and alert the bank if tampering is detected.

- Reinforced casings and physical security measures help prevent physical attacks and unauthorized access to the device’s internal components.

7. Software security

- Regular software updates are essential for patching vulnerabilities and closing security loopholes that could be exploited by hackers.

- Antivirus software and intrusion detection systems are also implemented to protect against malware and network threats.

8. Compliance and standards

- Micro ATMs are required to comply with various technical specifications and security standards set by regulatory bodies, such as the National Payments Corporation of India (NPCI) and the Indian Banks’ Association.

- Compliance with the Payment Card Industry Data Security Standard (PCI DSS) is also crucial for securing cardholder data and preventing financial crimes.

By implementing these robust security features, micro ATM provide a safe and reliable banking experience for users, particularly in areas with limited access to traditional banking infrastructure.

Role of Micro ATM in Financial Inclusion

Micro ATMs are small, portable devices that enable basic banking services, playing a significant role in fostering financial inclusion, particularly in areas lacking traditional banking infrastructure.

Here’s how Micro ATMs contribute to financial inclusion:

1. Expanding accessibility and convenience

- Bridging the rural-urban gap: Micro ATMs extend banking services to remote and rural locations, bridging the financial services gap between urban and underserved areas.

- Doorstep banking: These portable devices allow banking correspondents or agents to offer services directly in villages or local communities, eliminating the need for long and potentially expensive trips to distant bank branches.

- Serving the unbanked and underbanked: Micro ATMs facilitate access to the formal financial system for individuals who previously relied on cash or informal channels, enabling them to open accounts and conduct basic transactions.

2. Promoting essential banking services

- Cash withdrawals and deposits: Users can easily withdraw or deposit cash at their local Micro ATM point, reducing reliance on physical cash and potentially improving safety.

- Balance inquiries and mini-statements: Customers can conveniently check their account balances and review transaction history, promoting better financial management.

- Fund transfers: Micro ATMs enable secure and convenient fund transfers between accounts, facilitating remittances and other transactions.

- Government benefit disbursement: Micro ATMs streamline the distribution of government subsidies, pensions, and other welfare payments directly to beneficiaries’ accounts, enhancing transparency and efficiency.

3. Fostering financial and digital literacy

- Increased engagement with digital services: By using Micro ATMs for transactions, individuals gain familiarity with digital interfaces and basic financial concepts, increasing their comfort level with digital payments and potentially paving the way for broader adoption of digital financial services.

- Empowering communities: Enhanced financial literacy can empower individuals and communities to make informed decisions about their finances, potentially leading to improved financial well-being and economic opportunities.

4. Economic impact and entrepreneurial opportunities

- Supporting local businesses and economic growth: Micro ATMs stimulate local economies by facilitating cashless transactions and providing additional income streams for local merchants who act as banking agents.

- Creating employment: Operating Micro ATM provide employment opportunities for individuals in rural areas, further supporting local economic development.

- Potential for credit access: Data collected through Micro ATM transactions can potentially assist banks in assessing the creditworthiness of rural customers, potentially increasing access to loans and other financial products.

Micro ATMs are key drivers of financial inclusion by making banking services more accessible, convenient, and affordable for individuals and communities, especially in underserved areas. They not only simplify basic banking transactions but also empower individuals with financial knowledge and create new opportunities for economic growth and development, playing a vital role in building a more financially inclusive society.

Integration of Micro ATM with Banking Systems

Micro ATMs are portable devices that serve as mini banking outlets, primarily enabling basic financial services like cash withdrawals, balance inquiries, and mini statements, especially in remote and rural areas with limited access to traditional bank branches. Their integration with banking systems is crucial for fostering financial inclusion and empowering underserved communities.

Here’s a closer look at the integration process and its various facets:

How Micro ATMs integrate with banking systems

- API Integration: Micro ATMs connect to core banking systems (CBS) through Application Programming Interfaces (APIs), enabling secure and real-time data transfer between the device and the bank.

- Authentication Mechanisms: Micro ATMs use various authentication methods for secure transactions, including:

- Aadhaar Enabled Payment System (AePS): This utilizes a customer’s Aadhaar number and biometric authentication (fingerprint or iris scan) to perform transactions.

- Debit Card and PIN: Customers can also use their debit cards and enter their PIN for transactions, similar to traditional ATMs.

- Transaction Flow:

- A customer requests a transaction (e.g., cash withdrawal) from a banking correspondent (BC) equipped with a Micro ATM.

- The BC enters the customer’s details (Aadhaar or debit card information) and captures their biometric data or PIN.

- The Micro ATM sends the transaction request to the bank’s system via secure APIs.

- The bank verifies the customer and transaction details, and if approved, the transaction is processed.

- The BC dispenses cash (for withdrawals) and provides a receipt.

- Intermediaries and Micro ATM Providers: Businesses and financial institutions often partner noble web studio with Micro ATM service provider to handle the deployment, maintenance, and technical support of these devices. These noble web studio also offer integration with various digital solutions, including AEPS, BBPS (Bharat Bill Payment System), and mobile recharge platforms.

Benefits of integration

- Increased Financial Inclusion: Micro ATMs extend banking services to remote and underserved areas, bringing millions into the formal banking system and empowering individuals and small businesses.

- Convenience and Accessibility: Customers no longer have to travel long distances to access banking services, saving time and costs.

- Cost-Effectiveness for Banks: Micro ATMs are cheaper to deploy and maintain than traditional ATMs, enabling banks to expand their reach with lower operational costs.

- Employment Opportunities: Micro ATMs create new job opportunities for local banking correspondents who operate these devices.

- Support for Government Schemes: Micro ATMs facilitate the efficient disbursement of government subsidies, pensions, and welfare payments, reducing leakages and ensuring beneficiaries receive their entitlements.

Challenges and solutions

- Connectivity Issues: Poor network coverage in some areas can hinder transactions. Software developers are improving Micro ATM software to ensure smooth operation even in low-bandwidth regions, with features like offline transaction support.

- Agent Training and Customer Awareness: Ensuring banking correspondents are well-trained and customers are educated about Micro ATM functionalities and security best practices is crucial for successful adoption.

- Security Threats: While Micro ATMs employ security measures like encryption and biometric authentication, risks such as skimming, data vulnerabilities, and social engineering attempts exist. Following best practices, like covering the PIN pad and regularly changing the PIN, can help mitigate these risks.

The integration Micro ATM with banking systems is a powerful driver of financial inclusion and digital empowerment, especially in remote and rural areas. By addressing challenges like connectivity and agent training, and by leveraging technological advancements, Micro ATMs will continue to play a vital role in India’s journey toward a cashless and inclusive economy.

How Micro ATM Machines Work: Step-by-Step Process

Micro ATMs are compact, portable devices designed to bring essential banking services to areas where traditional banking infrastructure is limited, particularly in rural and underserved regions. These devices are typically operated by authorized agents or Business Correspondents (BCs) who act as intermediaries between banks and customers.

Here’s a breakdown of the Micro ATM work process:

1. Connecting to the banking network

- Micro ATMs connect to the bank’s core banking system via GPRS, 3G, or 4G mobile data connectivity. This allows for real-time processing of transactions, even in areas with limited or unreliable internet access.

2. Customer identification and authentication

- Customers can initiate a transaction by providing their Aadhaar number or swiping their debit card.

- For Aadhaar-based transactions, the customer’s identity is verified using biometric authentication (fingerprint scan) against the UIDAI database.

- For debit card transactions, the customer enters their PIN for verification.

- In some cases, customers may also authenticate using a combination of Aadhaar and OTP, or magnetic stripe card and OTP, or magnetic stripe card and bank PIN.

3. Selecting the desired transaction

- Once authenticated, the customer selects the desired transaction type from the Micro ATM menu, such as cash withdrawal, balance inquiry, or fund transfer.

- For cash withdrawals, the customer enters the desired amount to be withdrawn.

4. Transaction processing and approval

- The Micro ATM transmits the transaction request to the bank’s server through the established network connection.

- The bank verifies the transaction details, including account balance and authenticity, and sends an approval or rejection message back to the Micro ATM.

5. Completing the transaction

- If the transaction is approved, the BC or agent dispenses the requested cash (in case of withdrawals) and provides the customer with a transaction receipt.

- Both the customer and the bank receive a confirmation of the transaction.

6. Security measures

- Micro ATM transactions are generally secure and incorporate features like encryption of PIN data and biometric verification to protect against fraud.

- Point-to-Point Encryption (P2PE) can be utilized to encrypt card data as early as possible and maintain encryption throughout the system, reducing the risk of data compromise.

In essence, Micro ATMs function as portable banking access points, enabling customers in remote areas to perform basic banking services with the assistance of a BC or agent, thereby significantly contributing to financial inclusion initiatives.

Future Trends in Micro ATM Technology

Micro ATMs are transforming financial access in remote and underserved areas, particularly in developing nations like India.

Here’s a look at some key future trends shaping micro ATM technology:

- Cloud-Native Architecture and AI-powered Transaction Monitoring: Expect a shift towards cloud-native software architecture for real-time data processing, seamless scalability, and secure backups, according to Vocal. AI integration will enhance fraud detection, transaction scoring, and user behavior analysis, improving security and reducing risks.

- Unified Financial Services Platforms: Modern micro ATM software is evolving into unified platforms offering a broader range of services beyond cash withdrawal and balance inquiries, such as AEPS service, money transfer service, BBPS service, PAN card services, and mobile recharge service. This multi-service approach increases revenue potential for agents and provides better service to users.

- Advanced Biometric Authentication: Beyond fingerprint recognition, expect to see the adoption of iris scans and even facial recognition in pilot stages for enhanced security and convenience.

- Offline Transaction Capabilities: Addressing internet access challenges in remote areas, micro ATM developers are building offline-first architectures that store transactions locally and sync with the server when network access becomes available.

- Multilingual and Voice-Enabled Interfaces: To cater to diverse user bases, micro ATMs are offering multi-language support and experimenting with voice-enabled instructions for increased accessibility, especially for visually impaired users or first-time digital customers.

- Enhanced Agent Dashboards and Analytics: Expect more customizable dashboards for agents, providing them with better tools for mission tracking, customer transaction history, settlement reports, and wallet balance overviews.

- Blockchain for Data Integrity: Blockchain technology is being explored to enhance data integrity and transaction verification in micro ATM systems, offering secure, timestamped, and tamper-proof data.

- White-Label Solutions: The B2B fintech market is seeing a rise in white label micro ATM software, allowing businesses to launch branded solutions, manage agent networks, and customize features.

- Focus on Compliance and Security: With increasing regulations and the need to protect sensitive financial and personal data, compliance with regulations like GDPR and India’s DPDP Act, and robust security protocols, including data encryption and tamper detection, are paramount for micro ATM development. AI-based fraud detection and risk management will be crucial for prevention.

- Integration with Digital Wallets and Wider Banking Services: Expect micro ATMs to seamlessly integrate with digital wallets, enabling wallet-to-wallet transfers and QR code payments. They may also expand to offer services like loan disbursement and micro-insurance, further increasing their value to communities.

- Improved Connectivity and Reach: Advancements in internet infrastructure, particularly in rural areas, will improve the efficiency and reliability of micro ATM services, boosting financial inclusion.

- Collaboration between Fintechs, Banks, and Governments: Successful financial inclusion through micro ATMs depends on collaborative efforts between technology providers, financial institutions, NGOs, and government bodies.

- AI-driven Predictive Maintenance: AI can analyze ATM usage patterns and sensor data to predict potential hardware failures, minimizing downtime and maintenance costs, says ATM Industry Association.

In essence, future micro ATM technology aims to be more intelligent, secure, versatile, and seamlessly integrated into the evolving digital payment ecosystem, ultimately expanding financial access and empowering underserved communities.

Choosing the Right Micro ATM Provider

Selecting the best micro ATM provider like Noble web studio depends on your specific needs and priorities, particularly if you’re looking to operate in India’s diverse financial services landscape. Here’s a breakdown of key factors and prominent micro atm providers to consider:

Key factors to evaluate

- Cost and Investment: Compare initial device costs, recurring service fees, and commission structures to ensure profitability.

- Transaction Limits and Features: Examine daily/per-transaction limits, available services (cash withdrawal, balance inquiry, fund transfer, mini statements, etc.), and support for Aadhaar-enabled payment systems (AEPS).

- Ease of Use and User Interface: Prioritize intuitive software, multi-language support, and user-friendly devices for both agents and customers.

- Security and Reliability: Verify compliance with regulatory standards (e.g., PCI DSS), biometric authentication (Aadhaar or fingerprint), robust encryption, and robust hardware for durability.

- Customer Support and Training: Assess the noble web studio support system, including technical assistance, training programs for agents, and resolution times.

- Connectivity and Technology: Evaluate connectivity options (GPRS, 3G, 4G, Bluetooth, Wi-Fi), real-time transaction processing, and integration capabilities with existing banking systems.

- Scalability and Future-Proofing: Choose a Noble web studio that offers scalable solutions and supports integration with other payment solutions to accommodate future growth.

- Reputation and Reviews: Research the Noble web studio customer reviews, and testimonials to gauge reliability and customer satisfaction.

Noble Web Studio Leading Micro ATM Provider in India

- Noble Web Studio Offers comprehensive solutions, including devices, software, mobile applications, and attractive commissions on cash withdrawals.

- Known for affordable devices, high commissions, and a wide range of Aadhaar-enabled services.

- Noble Web Studio Provides user-friendly platforms with high commissions on cash withdrawals, along with training and marketing support for agents.

- Maintains an extensive network of local retailers for wide reach, featuring a user-friendly interface and additional services like mobile recharges and bill payments service.

- Focuses on serving rural and semi-urban areas through a growing network of agents, aiming to increase financial inclusion.

Important considerations

- Location: Evaluate the availability of network coverage and support services in the areas where you plan to operate.

- Target Audience: Consider the specific needs of your target customers when choosing features like biometric authentication and language support.

- Business Model: Determine if your business model aligns with the provider’s commission structure and available services.

How to Choose the Right Micro ATM Machine for Your Business

Selecting the right micro ATM machine involves considering various factors to ensure it aligns with your business needs and provides a good return on investment.

Here’s a breakdown of the key considerations:

1. Ease of use and user-friendly interface

- For both you (the business owner/operator) and your customers: The micro ATM should be simple and intuitive to operate.

- Target audience: Especially crucial in areas where customers may have limited familiarity with banking technology, a user-friendly interface enhances accessibility and reduces potential frustration.

- Language support: Consider devices that support multiple languages if your customer base is diverse.

2. Security features

- Protecting sensitive data: Robust security measures are crucial when dealing with financial transactions.

- Authentication methods: Look for devices with secure authentication like Aadhaar biometric verification or PIN-based systems to ensure only authorized individuals can access services.

- Compliance: The noble web studio should adhere to industry security standards and regulations, such as PCI DSS, for sensitive financial data protection.

3. Reliability and uptime

- Minimize downtime: Choose a noble web studio with a high uptime record and a reputation for minimal service interruptions, as downtime can lead to significant losses.

- Consistent performance: The machines should be able to process transactions consistently and reliably.

- Maintenance support: A strong maintenance and support system in place is essential for quick repairs and minimal disruption to your services.

4. Customer support and training

- Comprehensive support: Ensure the micro atm provider like noble web studio offers excellent customer support to assist with technical issues and provide necessary guidance.

- Staff training: Training for your staff on operating the devices and basic troubleshooting is vital.

- Multiple support channels: Look for noble web studio who offer support through various channels like phone, email, and potentially on-site assistance.

5. Cost and pricing

- Affordability and value: The pricing model should align with your budget and offer a competitive return on investment.

- Transparency: Seek transparent pricing with no hidden costs.

- Transaction fees: Compare transaction fees offered by noble web studio to maximize profitability.

6. Scalability and future-proofing

- Grow with your business: Choose a best micro atm solution that allows you to expand your services as your business grows.

- Integration with other payment solutions: Consider whether the micro ATM integrate with other digital payment methods like mobile payments and QR codes.

7. Reputation and reviews

- Due diligence: Research the noble web studio reputation, read customer reviews, and check for any past issues or complaints.

- Reputation as an indicator: A good reputation signifies reliability and customer satisfaction.

These factors, you can make an informed decision when choosing the best micro ATM machine for your business and effectively enhance your service offerings and profitability.

Conclusion: The Growing Role of Micro ATM Machines in Digital Banking

Micro ATM machines have made banking services more accessible, especially in rural and remote areas. With features like fingerprint authentication, instant balance checks, cash withdrawal, and Aadhaar-enabled payments, Noble web studio offer a smart solution for users without regular access to banks. For small businesses, retailers, and banking agents, Micro ATMs are a reliable way to offer essential financial services with low setup costs.

At NobleWebStudio, we provide secure and easy-to-use Micro ATM solutions that help you serve your customers better. Whether you’re starting a fintech business or expanding your current services, our technology is built to support you every step of the way. Start growing your digital banking business today with NobleWebStudio’s trusted Micro ATM services.

FAQs: Essential Features of Micro ATM Machines

Ans. A Micro ATM is a small, portable device used by banking agents to help customers withdraw cash, check balances, and make payments using their debit card or Aadhaar number with fingerprint verification. It brings banking to your doorstep.

Ans. Anyone with a bank account can use a Micro ATM. It’s especially helpful for people in rural areas where traditional ATMs and bank branches are not easily available.

Ans. Micro ATM machines offer essential features like:

Cash withdrawal

Balance inquiry

Mini statement printing

Aadhaar-enabled transactions

PIN or biometric-based access

These features make banking quick and secure for users.

Ans. Unlike large ATMs, Micro ATMs are compact and mobile. They don’t need to be installed in a fixed location. Agents carry them and connect through mobile networks to provide banking services in remote or low-infrastructure areas.

Ans. Yes, Micro ATM transactions are very safe. They use encryption, OTPs, and biometric authentication (like fingerprints) to make sure your money is secure.

Ans. Absolutely! Micro ATM devices provided by NobleWebStudio are designed to work with all major Indian banks, ensuring flexibility and convenience for customers across the country.

Ans. Getting started is easy. Just visit NobleWebStudio’s official website, fill out a quick form, and our team will get in touch with you. We provide full setup support, training, and after-sales service.

Ans. At NobleWebStudio, we offer trusted, tested, and affordable Micro ATM solutions with fast setup, 24/7 support, and top-quality software integration. Our goal is to help local agents and shop owners grow their income by offering banking services to their customers.